Legacy modernization

Enterprise modernization for insurers

Few leaders in insurance need convincing of the potential of embedded insurance — where insurance products and services are integrated into a business's offerings. Driven by convenience, personalization, and data-driven risk management, it offers a unique opportunity for insurers to bridge the 'protection gap' – the disconnect between customer needs and coverage. According to some estimates, spending on EI will grow from $63.1 billion in 2022 to $482.8 billion by 2032, a CAGR of 22.6%

Despite this potential, many of the early adopters have begun to realize some of their initial assumptions make it harder to succeed. Here, we present a framework for Embedded Insurance 2.0, which redefines insurance as more than just a revenue model and aims to enrich the entire value chain and daily experiences by forging strategic partnerships within the ecosystem. The EI 2.0 differential emphasizes:

Continuous research for new EI opportunities and conversion.

Seamless EI infusion for improved conversion and experience, informed by behavioral archetype studies.

Leveraging customer data for enhanced onboarding, servicing, and engagement

Efficient operations and processing.

Monetizing data for new capabilities and revenue channels.

Platform power for scalability and outreach (multi-channel compatibility, localization, etc.).

Embedded Insurance 2.0 transforms insurance into a value-enhancing ecosystem, with some commentators predicting that 30% of all insurance transactions will likely occur within embedded channels, in the next five years.

This article delves into the challenges insurers encounter when adopting Embedded Insurance models and explores essential considerations for effectively addressing these challenges.

Aspect |

Embedded Insurance 1.0 |

Embedded Insurance 2.0 |

Focus |

Add-on insurance at the point of sale |

Enhancing customer experience by embedding insurance in a day in life across the value chain by partnering with other industry partners |

Product Offering |

Generic, one-size-fits-all coverage |

Personalized, tailored to specific needs |

Value Proposition |

Convenience and additional revenue stream |

Improved and hassle-free overall customer experience: Sales -> policy servicing -> claims, and new revenue streams |

Partnerships |

Simpler Partnerships, less focus on co-creation |

Uplifting partnership value with data insight exchange, data monetization, and co-branding leverage |

Technology |

Integration for quote, and policy purchase APIs for the insurance products |

Extensive use of data analytics and AI for risk assessment, pricing optimization, and personalized offerings, for improved efficiency and customer engagement across the insurance value chain |

Design |

Business-driven and paper-based journeys |

Seamless, simplified & omnichannel experiences for convenient process and easy comprehension; catering to both self-service and assisted journeys. |

Example |

Travel insurance is offered at the airport during check-in |

Pay-per-mile car insurance: Integrated with ride-sharing platforms. Insurance cost adjusts based on actual miles driven and driving behavior.

|

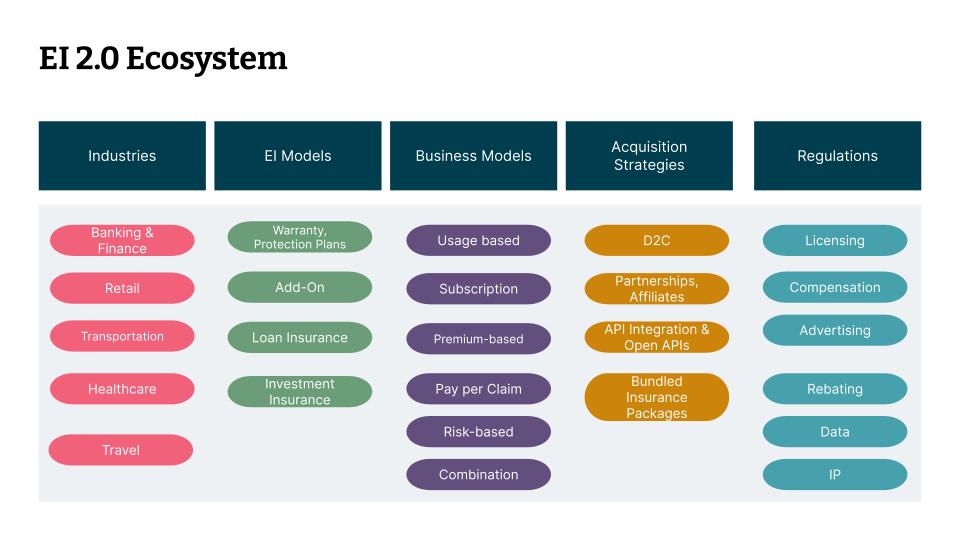

EI 2.0 fosters a dynamic ecosystem where various industries converge. Retail, travel, mobility, banking and finance, and even healthcare can all partner with insurance companies to offer seamlessly tailored insurance solutions within their existing customer journeys. This creates innovative business models like usage-based (pay-as-you-go ), subscription, micro-insurance, personalized product protection plans, etc. Acquisition strategies are based on data-driven insights and open APIs to target specific customer segments within their partner platforms. Meanwhile, regulations evolve constantly to address data privacy concerns and ensure fair competition within this rapidly growing ecosystem. Platform and technology muscle with simplified design allows scale, inclusion, and sustenance in the overall ecosystem.

So how might this play out? Consider the example of an elderly, philanthropist, who we’ll call Sam Curren. He’s busy even in his retirement life with assisting seniors like himself with wealth management advice and being a travel enthusiast. He seamlessly moves from being a hardcore professional to leading a well-balanced retired life with his passions leading the way.

A planned trip with his friends to the base camp of the Himalayas, there was no shortage of planning. He had his comfort clothing, hiking equipment, medicines, and all his IDs required for the trip. This was his first-time venture into the Himalayas and being an adventurous and fit person, he had it all well planned out with his blood pressure and diabetes medicines.

On the second day, when the troupe had reached halfway to the base camp, he started experiencing fatigue, tightness in his chest, and breathlessness.

There are many like Sam out there, who want to live and work in the moment and would rather focus on living their lives rather than do the heavy lifting of insurance, med-care, etc. What if the insurance companies, healthcare organizations, travel, and technology all worked together to take care of Sam and his needs, especially in times of crisis?

We can use this example to understand the future of embedded Insurance EI 2.0 in a transformed healthcare journey.

Embedded health insurance can be seamlessly woven into your daily life. Wearables proactively monitor your health, detecting abnormalities and triggering effortless doctor consultations — no appointments needed. Transportation to hospitals or diagnostic centers is pre-arranged, and costs for each step, covered by embedded insurance, are transparently displayed upfront.

This future eliminates the hassle associated with healthcare, especially during a traumatic situation. Businesses benefit from increased patient engagement, streamlined operations, and new revenue opportunities. Secure data management and clear cost breakdowns foster trust within the ecosystem. This reimagined future, (see below), benefits everyone: a proactive, empowered, and transparent healthcare journey.

In adopting embedded insurance business models as illustrated above, insurance companies face critical challenges such as: navigating complex regulatory landscapes, forging strategic partnerships with diverse industries, ensuring data privacy and security in integrated ecosystems, adapting legacy systems to support real-time integration, and most importantly, onboarding and handholding the customers in this journey.

Let’s dive deeper into some of the challenges:

The unknown unknowns of insurance: GTM (product, process and awareness) are critical starting points. From a customer’s perspective, they must be aware and empowered to choose, and leverage, insurance in the way that they need. Information and processes are needed on what customers opt in for, the cost-benefit, how can they initiate the process on a need basis and how they navigate the journey. Without those basics, the rest of the themes and considerations won’t even come into effect

The fragile trust chain: A slow or complex frustrating claim processing experience by the insurer, or a negative experience booking a hospital or ambulance online, could damage trust in the entire ecosystem — from the wearable company, to the virtual health platform and the insurer.

Regulatory labyrinth: Telemedicine consultations and online pharmacy options might have varying regulations across regions. The insurer must ensure compliance with all relevant regulations when processing claims or offering healthcare options.

The compliance conundrum: Obtaining explicit user consent for data sharing is crucial throughout the journey. For example, consent is needed for the wearable to share data with the virtual health assistant, and for the doctor to share treatment details with the insurer for claim processing.

Security Fort Knox, but fragile within: Sharing a patient's medical data across multiple touchpoints (wearable, virtual assistant, doctor's platform, insurer) necessitates robust security measures to prevent data breaches. A security lapse at any point could expose sensitive health information.

The legacy monster: Legacy insurer systems might not be equipped to handle real-time data exchange for claim notifications, estimated approvals, or digital payments to hospitals. This can lead to delays and friction in the process.

Integration nightmares: Teleconsultation with a doctor needs to integrate with the patient's digital health record (PHR) and potentially the insurer's system for real-time access to medical history and insurance coverage details. A clunky integration could disrupt or even block the consultation flow.

Data silos and disconnect: A wearable might track medical data, but for the insurer to use it for risk assessment or personalized plans, it needs to seamlessly connect with the virtual health assistant and the insurer's systems.

Digital divide and accessibility: Not everyone has access to reliable internet connectivity, smartphones, or wearable devices. This digital divide could exclude certain demographics from participating in the embedded insurance journey, limiting inclusivity. For example, an elderly patient might not be comfortable using a wearable or smartphone app, hindering their ability to leverage the full benefits of the embedded insurance program.

Insurers should orchestrate the overall customer experience of the embedded insurance journey and not restrict it to the insurance product journey.

For this, the insurer should:

Conceptualize and build the EI platform as a product. They need to be aware of the behavioral archetypes of target customers, and partners in the value chain and preempt their needs, wants and backgrounds.

Invest in GTM and Adoption Success Measures.

Plan early for long-term goals such as scale, revenue models, customer outreach and brand emphasis.

We’ve seen first-hand how insurers can embark on this transformative journey, and drive value for themselves and all of their stakeholders in the ecosystem by leveraging digital platforms and product thinking. To get them kickstarted, we’ve developed COEVOLVE (COllaborative EVOlution — Customer Centric Partner Ecosystem with Open APIs), to enable insurers to identify important considerations for their embedded insurance strategy:

Stage 1: Partner ecosystem design

Strategic partner selection:

Action: Conduct thorough due diligence on potential “digital ecosystem” partners. Evaluate their technology and data stack, security practices, compliance expertise, and alignment with your company's values. Ensure that the partner is focused on outcomes and can make rapid decisions and execute rapidly.

Benefit: Reduced integration challenges, minimized security risks and a well-coordinated ecosystem that delivers a seamless user experience and can evolve.

Collaborative onboarding:

Action: Develop a clear and efficient onboarding process for partners (like web aggregators, fintechs, e-commerce players, super-apps, other industry partners, etc.), including API documentation, technical support and compliance guidelines. Consider partners as your internal customers and their success is the key to achieving the entire embedded insurance program milestone.

Benefit: Faster integration of new partners, in turn reducing time-to-market for embedded insurance programs and offering a more scalable ecosystem with overall good partner experience.

Stage 2: Customer-centric product thinking

Co-creation with your employees and partners :

Action: Customer-centric mindset: Treat the Embedded Insurance program as a distinct product with its own product roadmap, user journey mapping and performance metrics. Diligent capability choices, clear ROI definitions, and conceptualization for CFRs and product and platform architecture — all go a long way in ensuring your digital investments truly pay off. Prioritize user experience (UX) design throughout the entire journey. Assemble a team of partners who possess a product-oriented mindset.

Benefit: An Embedded Insurance program that truly adds value to the user experience, leading to higher adoption rates, customer satisfaction, and potential revenue growth for both the insurer and its partners.

Stage 3: Technology infrastructure and open ecosystems

Open ecosystem and APIs:

Action: Think of open APIs acting as secure bridges between your systems, wearables, virtual assistants and other partners. Standardized data formats like FHIR (Fast Healthcare Interoperability Resources), ACORD (Association for Cooperative Operations Research and Development), OpenID Connect, etc, ensure smooth information flow. Imagine a user's wearable data seamlessly feeding into the virtual health assistant for a teleconsultation, with real-time access to their medical history and insurance coverage details.

Benefit: Streamlined user experience, faster claims processing, and the potential for personalized insurance offerings based on real-time health data.

Stage 4: Regulatory navigation and risk management

Compliance as a Platform (CaP):

Action: Imagine a dedicated platform that automates compliance checks across all embedded partnerships. This "Compliance as a Platform" (CaaP) acts as a central nervous system, pre-configuring compliance rules based on regulations. This "Compliance by Design" approach eliminates manual checks, saves time and resources, and ensures you're always ahead of the curve. This can be designed and evolved in a scalable and future-proof manner through state-of-the-art architecture and planning.

Benefit: Reduced risk of non-compliance fines, and the agility to confidently offer embedded insurance in new regions.

Stage 5: Building trust and continuous improvement

Building trust through security and transparency:

Action: Prioritize robust security like bank-grade encryption and multi-factor authentication. Imagine complete transparency with users/customers — clear communication about data security practices and control over how their data is shared within the ecosystem.

Benefit: Empowered users who trust the embedded insurance journey, leading to higher engagement and customer satisfaction.

Fostering continuous innovation:

Action: Establish a culture of innovation, encouraging collaboration between internal teams (IT, legal, product) and external partners. Imagine a dynamic environment where new embedded insurance solutions are constantly being developed to address evolving customer needs and regulatory landscapes.

Benefit: A future-proof embedded insurance program that stays ahead of the competition, offering cutting-edge solutions that delight customers.

In conclusion, the adoption of EI 2.0 models can appear to be a mammoth task but this is a journey that can be customized and sliced out for organizations to progress cautiously with the right milestone-driven plan and governance in place. To address the challenges in evolving EI, insurers need to follow the path of “Continuous Discovery and Continuous Delivery” along with the adoption of the COEVOLVE framework while keeping the users and stakeholders at the center. This means rapidly iterating on innovative yet simple embedded insurance (EI) products, leveraging the power of data analytics while ensuring compliance through a "Compliance by Design " approach. Once the scaffold is created with a multi-dimensional approach of business, customer, product, and technology, the rest of the journey can smoothly evolve.

However, success extends beyond product development. Building a robust EI ecosystem with guided and encouraged change management is crucial. From the outset, insurers need to establish the right principles of partnership and platform.

This two-pronged approach, focusing on both product innovation and fostering a collaborative ecosystem, will unlock the true potential of EI 2.0. It paves the way for a future where insurers, partners, and customers all benefit.