Security

Part 2: Understanding the implications of Open Banking on the consumer

In Australia, the Consumer Data Right (CDR) will go a long way in giving consumers trust, choice and control over sharing their personal data, but the CDR rules alone are only one part of the ecosystem. In the short term, it will be the role of financial institutions to implement the CDR through building a consent model to be used by their customers, partners and third parties.

During the course of our research, we discovered that many consumers share common feelings of skepticism, ambiguity and inertia around data sharing. We hope that the approaches discussed below will go some way in moving Australian consumers from passive to active data sharers, enabling the promise of Open Banking, and beyond to ‘Open Life’, a term that describes a future where consumers will have complete control of their data beyond banking to other open data verticals such as energy, telecommunications and even retail.

The Consumer Data Right was introduced by the government in August 2019 to provide Australians with the ability to share their personal data with businesses easily and securely in exchange for valued services. It aims to provide common data standards, with accredited third parties having the ability to access an individual’s data via application programming interfaces (APIs).

This new way of data sharing provides limitless opportunities for organizations to deliver richer, more personalised customer experiences than ever before. By accessing specific customer data, organizations can offer better deals and innovative products and services that are more relevant to consumer needs, convenient and highly secure, providing an incentive to switch.

In order to design a consent model we need to first understand what ‘consent’ means. In the context of the CDR, the Australian Competition and Consumer Commission (ACCC) outline that consumer consent must be “voluntary, express and informed and specific as to purpose, time limited and easily withdrawn”. However this is not how data sharing works in Australia today. The CDR aims to change this by giving consumers choice and control over their personal data, making them more informed than ever before.

CSIRO’s Data61 was appointed by the Australian Treasury as the Data Standards Body (DSB), to develop standards that will enable consumers to give consent to share and manage their data between parties. Thoughtworks, in partnership with advisory firm Greater Than X, supported the DSB in a Consumer Experience stream of work to design an online consent experience that takes into account the rules of the Consumer Data Right.

The focus of our work was to design a consent model that will bring choice and control to data sharing and improve the propensity for consumers to share their personal data. During the initial phase of research, we sought to understand current attitudes and behaviours towards data sharing and what encourages or attracts people to be more active in sharing their personal data. We also studied how people think and feel about the new, proposed way of sharing and what needs to be provided in order to build trust and give consumers control when consenting to share personal information. We conducted customer interviews and presented a prototype that allowed participants to interact with a consent interface that encompassed the CDR rules.

The consent model we designed was tested with 20 participants across metro and regional areas, representing a sample of potential early adopters of the CDR. These initial insights were then used to inform a second round of design and testing that informed the final report for the Data Standards Body and their stakeholders. This final report supported a set of Consumer Experience Guidelines that we hope will build an ethical and transparent data sharing ecosystem for both consumers and organizations alike.

We found that in today’s information economy, personal information is shared so often that many no longer reflect on what they’re sharing. Much of this behaviour is driven by the passive acceptance that it’s simply “the way it is”. During the customer interviews, we asked participants how much control they feel they have when sharing their data today. Using a likert scale, 1 - being no control and 7 - complete control, the results showed an average of 3.

Those who gave low scores felt:

Those who gave higher scores felt:

The second part of our research focused on the user interface (UI) of the consent model and understanding if the features, layout and language helped participants comprehend how this new way of data sharing will work and if they believe it provides them with choice, control and trust.

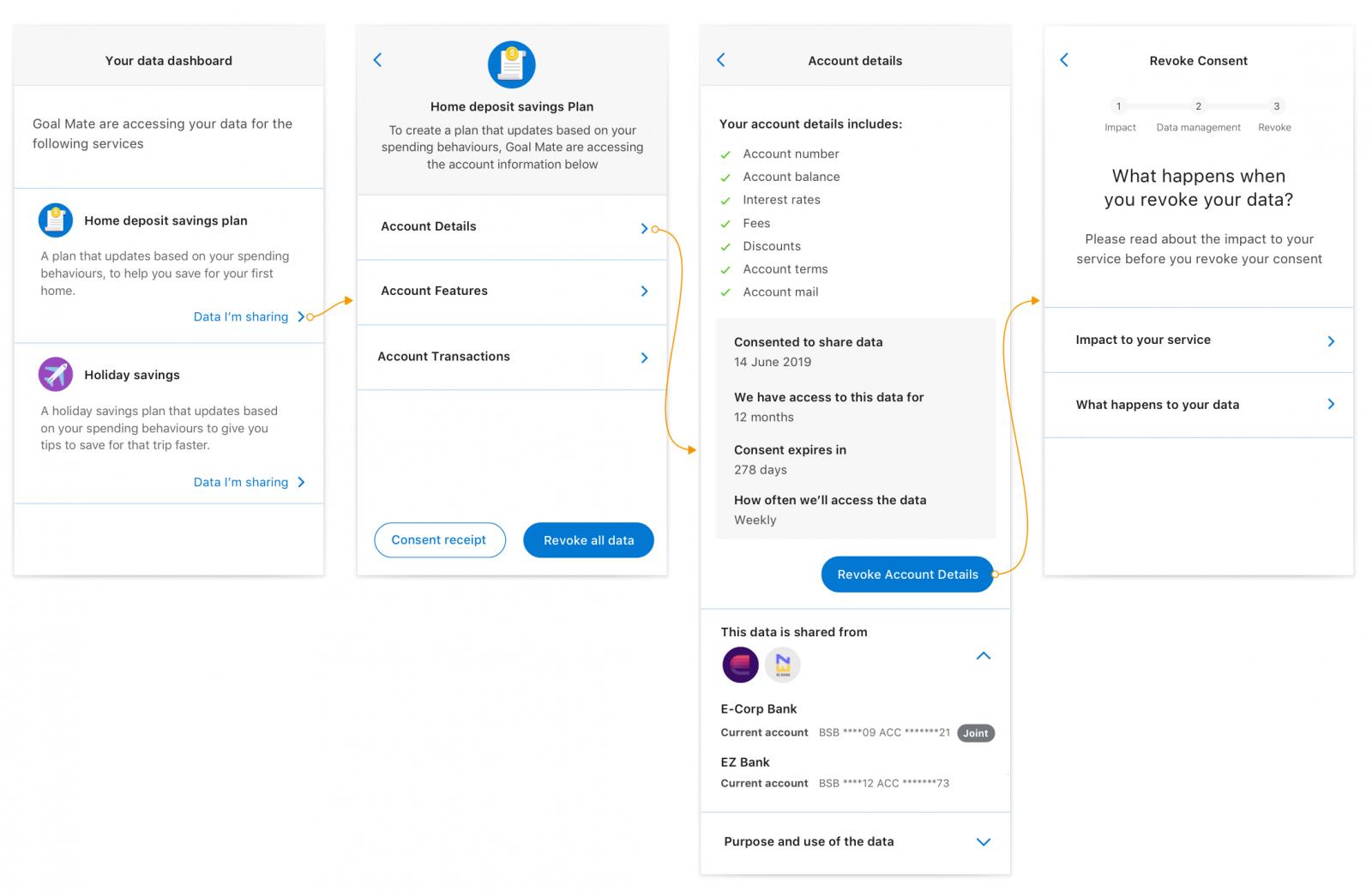

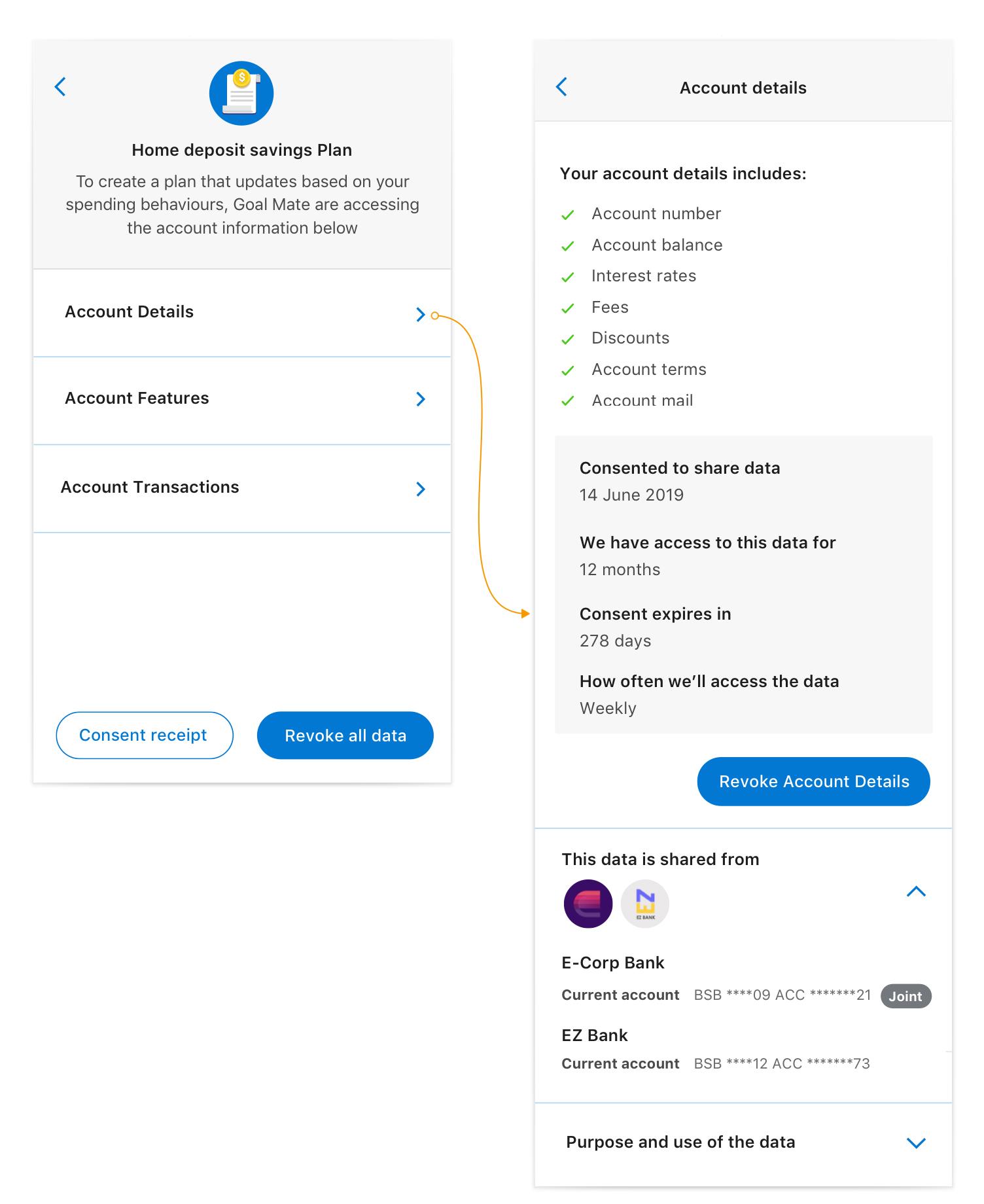

As stated in the CDR rules, consumers must be fully informed when consenting to share their data. Organizations must clearly state which data is being shared and the purpose for which the data is being used. We decided to utilise a progressive disclosure design pattern, which has been proven to focus the users attention by reducing clutter, confusion and cognitive overload. This meant each data cluster and its associated information was presented on a single screen. The consumer then had the choice to consent to that data cluster or not. We worked with the guiding principle that there should be no detriment to the consumer if they choose not to consent to share their data and we believe a basic level of product or service should be available regardless of their choice.

The consent experience also provided up front information about how long the data would be accessed and the frequency at which the data would be collected, ensuring the consumer was fully informed before they made their decision to consent.

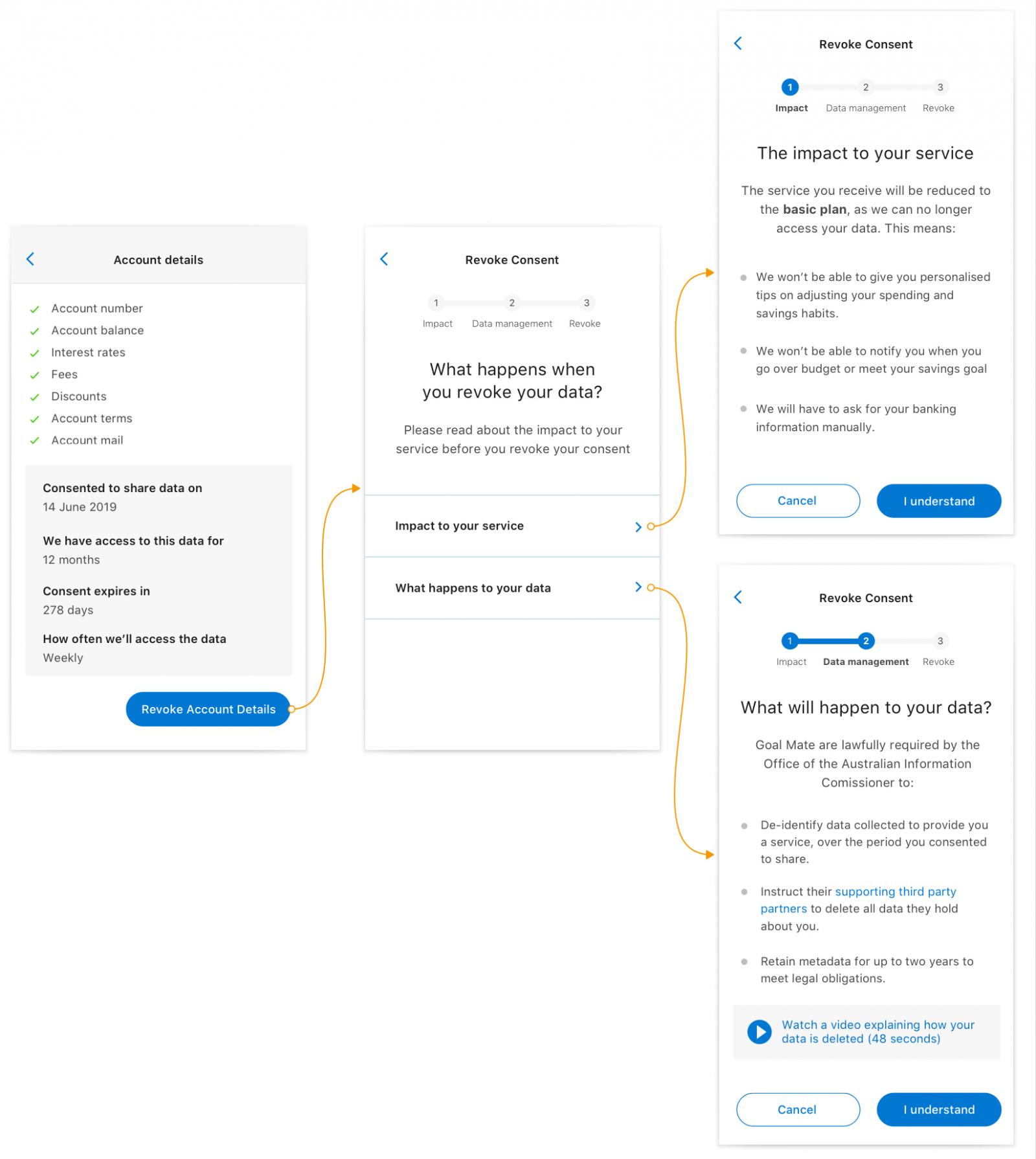

Withdrawing consent to share data, should also be fully informed. We believe consumers should be aware of the consequences of withdrawing, including the impact that it will have on their service, the specific data that they will no longer be sharing, the parties who no longer have access, and what will happen to their data. This transparency should leave participants with little concern from unanswered questions.

In round one of our research, we tested an assumption that including an ‘impact statement’ (i.e. a description of what may happen to a consumer’s service if their consent to data sharing is withdrawn) at the point of consent withdrawal would be sufficient to inform consumers of the consequences of no longer sharing their data. However we discovered that this statement alone was not enough and that consumers were still unclear on what happens to their data after they withdraw it, including data handling by supporting third parties. We addressed this by including a statement that explicitly outlines what happens to consumers’ data once it’s withdrawn.

We noted that whilst the data handling statement was now available, the way we structured the information on a single screen meant that information was competing with each other. Therefore, when we asked the participants to recall the consequences of withdrawing consent, their answers differed. To resolve this, we designed a third option that utilised the progressive disclosure pattern used in the consent flow, breaking down the ‘impact to your service’ and ‘what happens to your data’ into two distinct screens. Our assumption (which requires further testing) is that this will increase the consumers level of comprehension for both impact to service and data handling

Beyond withdrawing consent, most participants expected data to no longer be accessed, and any data stored by the accredited recipient to be deleted by them and their supporting parties. However there was skepticism as to whether the data is truly deleted and a lack of trust in organizations to do the right thing. The CDR gives explicit rules that data upon accreditation, suspension or withdrawal should be either de-identified or deleted. There is a need for transparency and clear articulation of how the organization chooses to handle the data, to instil greater trust in the process and ecosystem more broadly.

Under the CDR, accredited data recipients at a minimum must provide a CDR policy that includes any outsourced service providers e.g data processors, the nature of the service they provide and what CDR data is likely to be shared. It became clear during our research that it wasn’t obvious what relationship the outsourced service provider had with the accredited recipient. Participants felt uneasy at the idea that data could be carried across to an outsourced service provider and used against them to market unsolicited offerings. To alleviate these concerns we included an on-screen statement that clarified this relationship and how data will not be used for marketing purposes or any other reasons outside of the purpose statement of the CDR contract.

Beyond the consent model, financial institutions will need to build further trust by ensuring they deliver on the value they promise and provide consumers with transparency and greater assurance around security, in order to increase the propensity for them to share their personal information. The Treasury is currently developing a report into the future directions of the CDR and how it can further support a safe and efficient digital economy.

Financial services is only the first sector inline for the CDR with telecommunications and energy utilities up next, extending the possibilities of our consumer data rights and the control in which we can manage our Open Life.

Read more about the Consumer data right (CDR)

View the Consumer Experience: Standards and Guidelines

Disclaimer: The statements and opinions expressed in this article are those of the author(s) and do not necessarily reflect the positions of Thoughtworks.